- Title problems can occur from human error or fraud

- Defects in title are one reason why we use title insurance

- Title problems may not show up until after closing

- There are legal requirements to be able to sign a deed and not have it voided later

Get an as-is cash offer for your home

"*" indicates required fields

Title problems can make your home difficult to sell. Title problems, often called “title clouds” can occur even without a seller’s knowledge. In this article, we look at the most common title defects, and how to solve them.

Every property has a potential for errors in title

Every property has a history of owners. That history is called an ownership chain, or more often, a title chain. When a link in the chain has a problem, it’s called a title defect, or a cloud on title.

When purchasing a home, you may view title insurance as an unnecessary cost. However, title insurance provides protection for both the seller and the buyer against title defects. Title insurance, as the name implies, insures against property title defects or ownership defects. Some title problems may not become apparent for years. Others can hinder the sale of your home, and may even limit who you can sell your home to.

Imagine you are sitting in your beautiful, newly purchased home when you receive a letter from an attorney. The attorney says that you owe money to someone you have never heard of before. A long lost relative of the previous owner claims to be the owner of the home. Now, this relative wants his or her money for the sale of the home to you. The attorney is claiming that the seller should have known about the missing relative. Because their client didn’t sign the deed, they’re a part owner of the property with you.

Sadly, title problems like this are not unusual. It is a primary reason why people buy insurance to protect themselves from potential title claims.

Title problems caused by errors in public records

Believe it or not, not all public records are accurate. Just as credit reports may have errors, public records can too. These errors are often just simply typos and may seem trivial. However, these errors can create headaches for title transfers, and may even require legal help to resolve.

Incorrect Assessor’s Parcel Number or legal description

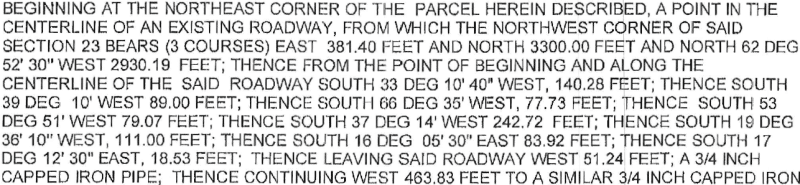

Most property in the United States has a Legal Description and an Assessor’s Parcel Number (APN) . The legal description is the language that defines the actual property location as a surveyor would describe it. It describes the property as being a certain distance, degrees and feet from a specified survey marker, or a certain lot shown on a recorded parcel or subdivision map. Typically, a legal description is the length of a paragraph. Most of us refer to our home by the street address. However, legally it’s the legal description that defines what you own.

Additionally, when land is subdivided into parcels for development, the county will assign a unique number to each parcel. This number is known as the assessor’s parcel number (APN). Your local government offices will use the APN to track property tax assessments and their payment.

Conflicts with the legal description

What happens if the legal description is in conflict with another part of the deed? Maybe the legal description conflicts with the APN or your street address due to a typo. When this happens, the legal description takes priority. If the legal description is wrong, it may require a surveyor to survey the property. If the APN or street number are incorrect, it may not matter. I’ve seen properties with multiple APNs and I’ve also seen street addresses that were on the wrong street.

Missing or incorrect/inconsistent names

Occasionally, title errors occur during document signing. During a divorce, attorneys may miss having the other party sign a deed. A title company may miss an heir who needs to sign documents to settle a probate. More commonly, a name may be misspelled, or the names between documents are not consistent. For example, one document may use a person’s middle initial, while the next document doesn’t. Generally, this would be immaterial and not affect the chain of title. But what if the middle names were different? If there were a difference in the middle name, this could result in a defective title.

Sometimes these can be solved easily by the closing attorney or title company with a corrected deed or signed affidavit. What happens if the person is unwilling to sign the affidavit or corrected deed? When this happens, it may require legal action known as quiet title. A quiet title requires bringing a lawsuit and obtaining a judgement from the court. Once the judgement is obtained and recorded, the title company can proceed with closing escrow.

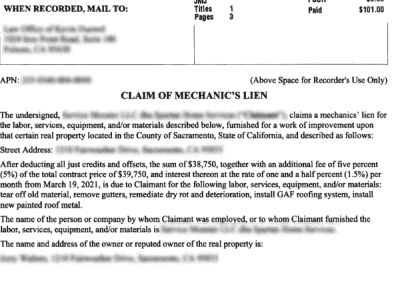

Title defects caused by liens

When a creditor is owed money, they can record a lien against your property. These liens may arise from medical bills, IRS liens, state or local property tax liens. There may also be contractor mechanics’ liens or a lien from your contractor’s material supplier.  If a creditor files a lawsuit and obtains a judgement against you, they can obtain an Abstract of Judgement against you. This creditor can then record the Abstract of Judgment against any property or home you own.

If a creditor files a lawsuit and obtains a judgement against you, they can obtain an Abstract of Judgement against you. This creditor can then record the Abstract of Judgment against any property or home you own.

Judgement liens in California last ten years, and can be renewed and last even longer. A recorded Abstract of Judgment and judgement lien stay with the property even if the property is sold to another party. Some creditors have been known to wait several years until the debtor shows any assets before recording their Abstract of Judgment. For these and other reasons, during a title company or closing attorney’s underwriting process, the name of each party in the sale of the home is examined for potential judgement liens that would need to be paid.

What happens to liens during foreclosure?

Liens recorded after the recording of your mortgage will typically be extinguished by the foreclosure. However, this is not always the case. There are some types of IRS and so called “super liens”, or UCC liens, that will not be wiped out by a foreclosure. For instance, in California we have PACER loans that are used by homeowners to do major home upgrades. These upgrades might include purchasing solar systems or new roofs and HVAC. These liens survive foreclosure, presumably because the new owner obtains the benefit of these upgrades.

Encumbrances cause clouds in title too

An encumbrance is when someone claims to have an interest in a property, besides the owner. This interest can be as simple as an easement. The easement might allow the utility company to drive on your property to get to their equipment. Or the encumbrance can be as severe as a lien preventing the sale of the property. Encumbrances can be held by parties with a financial interest in the home, such an IRS lien or a mortgage. Commonly, your local Home Owner Association and CC&Rs are an encumbrances against your property. In most states, any encumbrance that transfers with the property must be disclosed to the buyer. While an IRS lien may be paid off by the sale proceeds, HOA encumbrances will typically remain.

Preliminary title report

During escrow, your preliminary title report will reveal all encumbrances discovered. It’s important to read your title report as it will tell you what encumbrances stay with the property after closing.

Neighbor encroachments, easements

An encroachment is when you or your neighbor’s fence, driveway or building crosses the property line. However, your title company will probably not be able to identify these types of encroachments. If you suspect that the neighbor is encroaching on your property, you may need to hire a surveyor.

An easement is when someone has the right of access to cross your property. The neighbor who lives behind your new home may have had a gentleman’s agreement with a previous owner. The agreement allowed the neighbor in back to drive across your property in order to access their home. The agreement may not be recorded, even though it may have existed for years. These types of easements, called prescriptive easements, can be extremely difficult, if not impossible to remove.

Property line disputes

If you own rural property, your property lines may not be easily identifiable. Even if the property was surveyed, the surveyor may have made mistakes. We recently saw this on rural property. The property owner put a fence between his property and the neighbors using existing survey markers. The neighbor’s property sold years later after the fence was built. However, the new neighbor claimed the fence encroached onto his property. Now the new neighbor was demanding the entire fence be moved back 10 feet. The only way to resolve this dispute was to either move the fence, have the property re-surveyed or a quiet title action.

Even in long established subdivisions in urban areas, owners may not recognize boundary markers or property lines. We recently sold a home where the boundary line locations were unusual for the neighborhood. They identified our property as running all the way up against the neighbor’s home. What if we had tried to put a fence up following the boundary markers? It probably would have upset the neighbor since they would have lost a portion of their side yard. Additionally, some boundary markers may be destroyed or moved during construction. If we have rural land surveyed, we intentionally place additional markers back away from the edge of the road. This is so the county road equipment doesn’t destroy the property markers while maintaining their roads.

Missing heirs

Do you have a relative you haven’t spoken to in years? Not surprisingly, most families do. Sometimes, these family members can be completely missed during title searches, especially after the death of a parent. What if a home is sold, and a rightful heir later surfaces after the sale? This claim by an heir can create a cloud on title. Especially when the heir wants their share of the proceeds from the sale.

If a home is sold without title insurance, or transferred with a quitclaim deed, the new owner could be in for trouble. A typical escrow transaction involves title insurance and either a grant deed or a warranty deed. Both of these deeds guarantee the person signing has not transferred the property and that they are the owner. However, a quitclaim deed makes no guarantees. What if all of the heirs of an estate have not signed the quitclaim deed? The new owner may end up being co-owners with a missing heir. The missing heir may even sell their ownership rights to another party years later. In either case, you could end up being an ownership partner with people you don’t even know.

Lis pendens cloud title

A lis pendens is a public notice that a lawsuit has been filed against a property. It literally means, a suit as in lawsuit is pending against the property. The lawsuit may be triggered by many things. It can be triggered by a divorce, by the bank in the event of foreclosure, or a bankruptcy. I’ve seen lis pendens filed even by owners trying to prevent a foreclosure.

When a lis pendens has been recorded against a property, the suit must be settled before the property can be sold. If not, the lis pendens will transfer to the new owner. Lis pendens can take months, even years of legal costs before they it is settled. If a property has a lis pendens recorded against it, it may be years before the property can be sold.

If a seller sold a property with a lis pendens, the new owner becomes responsible for the lis pendens’ claim. This is why title searches are so important for buyers. Title searches by your title company verify that there are no legal filings against the property, or the seller.

A lis pendens can even be filed against the property after a “sale”. For example, what if you bought a property from an owner in bankruptcy. If the owner transferred the property without the consent of the bankruptcy court, they would be defrauding creditors. If this were to happen, a creditor of the former owner could record a lis pendens against the property, even after the property ownership was transferred.

Illegal deeds void title transfers

There are certain legal requirements for transferring title. Deeds that do not meet the legal requirements are called “void deeds”. In order for a property deed to be legally transferred, the following criteria must be met.

- The person must be not be judicially ruled as incapable of managing their affairs. For example, a person under the care of a conservator.

- Not a forgery, the deed must be signed by a legitimate owner. This is why most deeds are notarized.

- The deed cannot be signed by a minor (under 18 years old) unless person is emancipated.

- There cannot be conditions that must be met prior to delivering the deed to the grantee.

- The seller must specifically state who the deed is being granted to. For example, the grantee (new owner) name cannot be left blank, to be filled in later.

Forgeries and false impersonations

Obviously, a forged seller name or someone who has impersonated the owner is cause for deeds to become voided. While not required, most deeds are notarized by a neutral third party to validate a deed’s signatures. The notary validates the signer’s identity and signature to prevent fraud. The notary information may be part of the deed, or attached to the deed.

Conclusion – what to do if your home has title problems

The transferring of real property requires strict rules be followed to prevent fraud. When these rules aren’t followed, it can create flaws or clouds in the chain of title. Most transactions use a title company or title attorney, providing insurance against possible flaws in the chain of title. However, errors do occur and can be as simple as a missing signature, to a legal suit against the property. Does your home have a cloud on title? Go back to the company who processed your purchase to see what your title insurance policy will cover.

What if you are unable to clear the title problems? You may need to look to alternative ways of selling your home, while fully disclosing the title defects.