-

- There is less protection with quitclaim deeds than Grant or Warranty Deeds

- Quitclaim deeds are commonly used for transfers without title insurance

- Quitclaim deeds can make a property hard to sell in the future

- You cannot remove yourself from a mortgage by signing a quitclaim deed

Get an as-is cash offer for your home

"*" indicates required fields

Deeds are like the pink slip to your car. By signing them, you transfer your ownership to another person. There are many different types of deeds for transferring ownership of a property. However, if you aren’t careful, you can end up with a home that has a cloud or title defect making it hard to sell..

In this article, we look at quitclaim deeds and why they can be problematic for transferring title.

Different types of deeds for transferring property ownership

Before we look at quitclaim deeds, we want to understand the three primary types of deeds used for changing ownership.

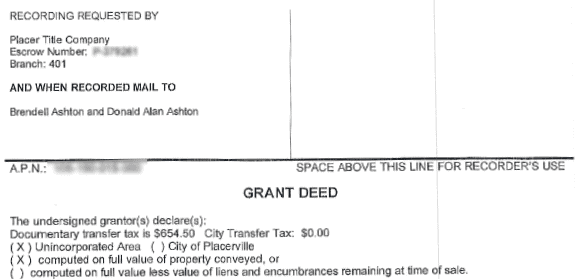

Grant deed

Grant deeds transfer ownership of a property. A grant deed conveys ownership to a new owner using language similar to “I hereby grant to new_owner”. This granting clause is where the term ‘grant deed’ comes from.

A grant deed includes two key guarantees to the buyer. First, the seller guarantees that the seller has not transferred the property ld to another person. However, it does not guarantee that the seller is the owner. Second, the seller guarantees there are no title flaws, such as liens or encumbrances, not disclosed to the buyer. These guarantees are not typically stated in the deed, but are known as “implied warranties“.

Most grant deeds are recorded in the public records of the county where the property is located. However, recording in public records is not required.

Because grant deeds are valid, even if not recorded, sellers must guarantee that there are no unknown sales. If there are other unrecorded deeds, they might affect the buyer’s interest. Your title insurance company can insure you against deeds that are recorded. However, it’s hard for them to know if a seller has secretly sold a property beforehand. Hence, the need for the first guarantee.

The second guarantee, protects the new owner from possible mechanics liens. These liens may be for recently completed work which the seller may not have paid their subcontractor for. They might also be for liens placed by their contractor’s suppliers. For example, when your roofer orders several thousand dollars of materials for your roof, but doesn’t pay the supplier.

Grant deeds are the most common type of deed found in public records in California. Most property transfers done by title companies in California, use grant deeds.

Warranty Deed

A warranty deed is similar to a grant deed except that it offers three guarantees to the buyer. First, it guarantees the property is not owned by someone else. Two, it guarantees there are no non disclosed liens or encumbrances. Three, it guarantees that the seller, also known as the grantor, will warrant and defend the title against any claims. This warranty defends buyers against any claims.

While warranty deeds can be used in any state, they are usually used in the Midwest and eastern United States. Warranty deeds are uncommon in California. This is due to our reliance upon title insurance to protect buyers, and to protect marketable title.

Quitclaim deed

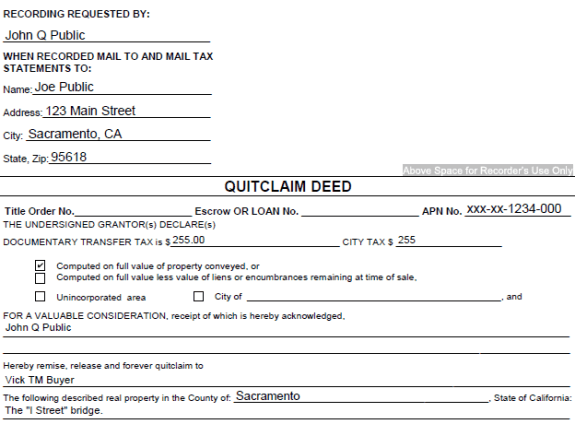

Unlike grant deeds and warranty deeds, quitclaim deeds offer no guarantees. They are similar to the proverbial statement about a person offering to “sell you the Brooklyn bridge”. A quitclaim deed transfers a person’s ownership interest in a property. However, there’s no promise that the seller owns the property. Nor is there a promise that they haven’t sold the property to someone else. And there’s no guarantee the property is free and clear of liens. If you’re going to buy a property from someone with a quitclaim deed, you need to do your homework. You need to be very thorough with your investigation and be willing to trust the seller blindly.

What is the purpose of a quitclaim deed?

Quitclaim deeds are common in inter family transfers of real estate. They common when family members want to avoid the costs of title insurance or attorney fees. They’re also commonly used when moving property in and out of a trust, such as during a bank refinance. Banks typically do not loan to trusts. Most banks require property ownership be under the name of real persons. So, before the bank will lend the funds, trustees may use a quitclaim deed to move the property ownership to a real person. Then, after the bank loan is completed, the trustee uses a quitclaim deed to move the property back into the trust.

Quitclaim deeds may also be used to transfer ownership between spouses, or ex spouses in the case of divorce. However, an inter-spousal grant deed is more common. In the event of a couple’s divorce, either of these deeds might be used to transfer the home entirely to one or the other.

Does a spouse have the right to property after signing a quit claim deed?

The short answer is “no.”. When a spouse transfers property after signing a deed of any type, they release their rights to the property.

What about when there are multiple owners, but only one borrower? Most lenders will require title to be vested in the name of the borrower as their “sole and separate property”. This mean the other owners, will need to be removed from title while the bank loan is being funded. Once the loan is completed, the owners can hire a deed preparation company or an attorney to put both parties back on title.

Repercussions of a quitclaim deed

Grant deed with title company stamp

Because quitclaim deeds can be so easily created, and recorded by anyone, they can be problematic. Normally, deeds recorded by title companies have a stamp identifying the title company responsible for creating and recording the deed. However, if a Joe Public decides to use a quitclaim deed to transfer ownership and not use a title company? This will indicate the lack of title insurance for the transaction. This doesn’t mean the deed is invalid, but it raises red flags to attorneys and title companies.

When a title company issues title insurance to a buyer, they follow strict rules regarding the creation of the deed. Because this process is managed by the title company, they are willing to offer the buyer insurance protecting the buyer from title problems. The title company will verify the current owner in addition to checking for any recorded liens against the property.

Date down title searches

Any property has likely been transferred many times over hundreds of years of history. In California, grant deeds go all the way back to the Spanish colony. It would be impractical (and repetitious) to examine a property’s title history back to the Spaniards. To make it easier, title companies simply look for the last recorded grant deed recorded by a title company. Then they look at all transactions after that date. This is known as a “date down search”.

If a title claim arises from a previous transfer insured by a previous title company, it’s the previous title company that’s responsible for the claim. The current title company is only guaranteeing transactions since the last insured transfer.

Quitclaim deeds can create clouds on title

However, what happens when there’s a deed without a title company stamp recorded between the current sale and the previous title company’s insurance policy? Who’s going to insure around this unknown deed? What happens when title companies encounter these situations? Often, they require the sellers to sign affidavits to release the title company for claims relating to the unknown deed. Or, in some cases they may not be willing to insure the property transfer. When this happens in the middle of your transaction, you may need to find a different title company.

Years ago I was involved in selling a property owned by a very complicated trust agreement. We were in the middle of escrow, when I received a call. The title company we were using said they couldn’t complete the transfer because of language in the trust. We had to change title companies in the middle of escrow to a company that understood the trust agreement.

Does a quitclaim deed remove me from the mortgage?

There was a common scenario during the Great Recession done by people in foreclosure. They assumed that if they signed a quitclaim deed over to someone else, they were no longer responsible for the mortgage. Others attempted to use quitclaim deeds to cloud title and try to prevent foreclosure. This was also futile and did little to prevent mortgage companies from foreclosing.

When a borrower signs documents for a home loan, they also sign either a mortgage or a deed of trust. These documents create a lien on the property that protects the lender in case of default. In the case of foreclosure, these documents take priority over any future transfers of ownership. The borrower, is still responsible for paying the loan back to the lender.

How to be removed from a mortgage

There are very few ways to be removed from a mortgage without paying it off One way, is to work with the bank to attempt a Deed in Lieu. A Deed in Lieu, is a special deed that transfers ownership of the property to the bank. In a Deed in Lieu, the borrower gives the lender the home, and the lender removes the borrowers mortgage. However, a Deed in Lieu does not provide any of the guarantees regarding protection from liens and encumbrances. For this reason, many lenders are hesitant to accept Deeds in Lieu.

Assuming the loan

Assumptions are another way that someone can be removed from a loan. Although we don’t see them in today’s market, assumptions are still allowed by lenders on FHA, VA loans and adjustable rate mortgages. An assumption allows the loan to be transferred to a new borrower. Assumptions were very common in the 1980’s when interest rates were high. If a seller had a loan with a lower interest rate than what the buyer could obtain, the buyer would take over the seller’s loan.

With an assumption, the new borrower applies to the lender to take over the current owner’s loan. If the lender accepts the assumption, the home can then be deeded to the new borrower. The previous owner is then removed from both the mortgage and property title. However, it’s not something we see these days because of low interest rates.

Selling a home with a quitclaim deed

Selling a home with a quitclaim deed is perfectly legitimate. However, if you understand the problems it creates for re selling the home, you can quickly see why it can create problems for the buyer in the future. You may truly own the property, and it may be free of liens and encumbrances. However, future title companies may not be willing to simply take your word for it.

It may be several years later before the buyer who obtained the quitclaim deed needs to sell the property. Does the current owner or title company still have a way to contact the prior seller? How do they verify the legitimacy of the sale? It not, this could create significant challenges for the latest owner to obtain title insurance selling the property.

Conclusion

In summary, the problem is not quitclaim deeds by themselves. It’s the lack of title insurance when seller’s transfer title between different parties that often accompanies quitclaim deeds. The same could be true even if a grant deed or warranty deed were used to transfer ownership, but without obtaining title insurance. However, in the case of grant and warranty deeds, there is at least an implied guarantee of ownership, and the property being free of liens and encumbrances.